Commentary: Rule 2 Nature of cover

2.1 General

This Rule sets out the nature and extent of the cover provided.

2.2 Rule wording constitutes framework of cover

The first paragraph of the Rule states that the cover provided by the Club is set out in these Rules. It means that the cover is no more and no less than expressed by the wording of the Rules. Extension of cover may be agreed on special terms. According to the definition in Rule 1, “agreed” means “agreed in writing”. It follows that any extension of cover must be agreed in writing by the Club to the Member concerned. When such an extension has been agreed and the special terms and conditions decided, the cover is still subject to all applicable general terms and conditions contained in these Rules.

In line with Swedish law, the Member has the burden of proving that a claim is covered.

2.3 Cover is for liabilities

The second paragraph of the Rule states that the cover is in respect of “liabilities, costs or expenses”.

The keyword is “liabilities”. The object of cover under the P&I Insurance is legal liabilities incurred or likely to be incurred by the Member under any legislation which is applicable to the case. It is not necessary for the liability to have been determined by a final court judgment or arbitrational award. It is enough that a legal evaluation of all known facts results in the conclusion that the Member is likely to be found liable or that possibility cannot be excluded. These decisions should be made by the Club, which has the responsibility for ensuring that payments are made only for risks covered by these Rules.

It follows that Members should not be compensated for payments or settlements made to please customers and retain commercial goodwill. The Club appreciates that claims are a reflection of the Member’s commercial relations and the Club endeavours in its handling of the claims not to harm those relations.

The words “liabilities, costs or expenses” appear in many clauses to describe the object of the cover. Some clauses provide cover only for costs or expenses. Then there is no liability to insure, only costs or expenses incurred by the Member. The Club also has an obligation to check the accuracy of costs or expenses in order to ensure that they refer to the purpose described in the clause.

The facts, documents and information required by the Club to take the necessary decisions on liability, cover and compensation are described in the comments to the individual Rules.

The liabilities covered may be based in negligence (in tort), on specific laws (statutory or regulatory) or in contract. The cover is for those liabilities which the Member has no legal means of avoiding. If liabilities are taken on unnecessarily, say, for commercial reasons, such risks should not necessarily be shared by the Members of the Club. This is in line with the concept of mutuality on which the P&I Insurance is based. Therefore, cover of contractual liabilities is subject to special conditions as described in these Rules.

The overarching principle is that the Member is expected to act as a “prudent uninsured”. Having insurance should not be a reason to act imprudently. The member should act prudently, at all times, firstly to avoid and secondly to minimise exposure to costs, liabilities and expenses which may be covered by the insurance.

The word “liabilities” implies that it should be in relation to third parties. No one is liable to compensate himself. Losses sustained by assets or property belonging to the Member can create a right to compensation only when expressly stated in these Rules.

2.4 Cover if for the Member

The second paragraph of the Rule makes it clear that it is only the Member who is covered. No party other than the Member is entitled to compensation under these Rules. The definition of a Member is stated in Rule 1. See comments under 1.4.4.

Although the cover is for the Member, the liabilities insured are mostly caused by negligence on the part of his servants. It may seem contradictory, but it is one of the basic principles of P&I Insurance that the Member is covered for his servants’ negligence but not necessarily for his own negligence (see comments under 11.1.3). However, his servants do not enjoy any cover of their own since they are not Members. In certain instances, however, the servants can be brought under the Member’s liability exclusion umbrella by a Himalaya clause (see comments under 4.1.7).

The cover for the Member does not generally include claims filed against the Member’s directors and officers personally since the P&I cover should not be viewed as a D&O cover for directors and employees of a Member. Instead, the concept of affiliation or association should derive from an ownership interest in the entered vessel. In terms of companies with many shareholders, cover extends to persons having a controlling interest and/or operational involvement in relation to the vessel.

The Rules do not allow a substitution of Member under the policy of insurance. That appears from Rule 27. See comments under 27.4.

Certain parties may enjoy the benefit of the cover under these Rules without being Members. That is also applicable for co-assureds under Rule 30, affiliated companies under Rule 32 and mortgagees under Rule 35. See comments under 30.3, 32.1 and 35.2 respectively.

Under certain circumstances, claimants may achieve a separate right to seek reimbursement for their losses direct from the Club by direct action. Direct action can be imposed upon the Club by international conventions adopted as domestic law. In some countries, claimants may be granted a right of direct action by laws not related to any convention. Claimants bringing a direct action against the Club should not be entitled to better rights than the Member. This view, however, is not unchallenged. For further comments on direct action, see under 2.9.

2.5 Cover is restricted to owner, operator and Bareboat Charterer risks

The P&I Insurance is not a general liability cover for the Member. In the performance of his business activities he may incur liabilities in a number of (non-shipowning) capacities, for example as the owner of warehouses, terminals, trucks and cranes or when acting as broker, stevedore or forwarding agent. For liabilities incurred in any such capacity, no cover is provided by the P&I Insurance, which is strictly vessel related. According to the second paragraph of the Rule, the cover is confined to those liabilities which the Member incurs as owner, operator or Bareboat Charterer of the entered ship. Cover for other charterers such as Time or Voyage Charterers is provided separately and laid down in a separate set of rules.

2.6 Cover is restricted to operational risks

The second paragraph of the Rule underlines that, in order to be covered, the liabilities must have been incurred during the operation of the entered ship. Operation means practical matters like loading, navigating, discharging and issuing freight documents. Liabilities resulting from business transactions such as violation of anti-trust regulations are not regarded as incurred during the operation of the entered ship.

2.7 Cover is restricted to direct consequences

Not all consequences of the liability risks insured are covered. When the Rules use the words “liabilities, costs or expenses” to describe the extent of cover, it means those which are a direct consequence of the operation of the entered ship. A serious longshoreman accident may have a number of side effects such as delay of the loading/discharging operations, with waiting time for gangs and vehicles: the ship may come off-hire; repairs of the ship and its equipment may be necessary to regain compliance with union and safety regulations. All these possible consequences are not necessarily covered simply because the liability for the main event, the personal injury, is covered. “Operation of ship” means the physical operation, such as the acts of loading, stowing and discharging cargo, navigating the vessel and caring for the cargo while it is on board the vessel, rather than the commercial aspects for which those activities are performed (such as the earning of hire or freight for profit).

This is emphasised by the words ”in direct connection with” in the second part of the clause. Different expressions may be used in the Rules to describe the requirement of a direct causal connection between the event and the liabilities, costs or expenses incurred by the Member for cover to be provided. In the Swedish wording which, according to Rule 1, shall prevail in case of a dispute, expressions like ”föranledd av” (trans: as a result of), ”till följd av” (trans: as a consequence of), ”på grund av” (trans: because of) or ”som orsakats av” (trans: caused by) are to be regarded as synonymous. They reflect the same demand for a direct causal connection as stated in Rule 2. Corresponding synonymous expressions in the English wording are ”as a result of”, ”as a consequence of” or ”caused by”.

Indirect consequences of an event are covered only if and to the extent it is so stated in these Rules. Examples of situations where indirect consequences of an event are covered can be found under Rule 4 Section 6 and Rule 7 Section 5.

To prevent situations from arising where the Member incurs liabilities for indirect consequential losses which are not covered under these Rules, the Member should contract on terms which expressly exclude liability for such losses in bills of lading, passenger tickets or other contracts entered into. See comments under Rule 10 Section 2.

2.8 Cover is restricted to events which occur during the period of insurance

According to the second paragraph of the Rule, the cover under these Rules is for liabilities, costs or expenses arising out of an event during the period of insurance. In other clauses or in circulars, words like “occurrence”, “accident” or “casualty” are used as synonyms of “event”. It is important to establish whether an event arose during the period of insurance, as that is a condition for cover. Therefore, the meaning of an event has to be defined.

For the purpose of these Rules, an event is an occurrence or casualty which may result in liabilities, costs or expenses for which a Member seeks compensation from the Club. Further qualifications for an event may follow from certain Rules (see for instance comments under 6.2.4).

In many cases the liability arises at the moment the event occurs. For example, the ship’s winch-wire snaps and a valuable piece of machinery is dropped on the quay and smashed.

In some cases, however, considerable time may elapse between the event and the liability. For example: a pipe passing through the hold is fractured or breaks but this does cause damage immediately; it only causes damage when it is filled with water a month later.

It often happens that no specific event can be identified. For example, if cargo is missing at the time of discharge it may be impossible to find out when and why it disappeared.

There can be a sequence of events, each of which impose separate liabilities. For example: a ship finds a stowaway on board in one port and the shipowner incurs costs to prepare his disembarkation; in a subsequent port the stowaway escapes, causing the immigration authorities to impose a fine upon the ship.

It follows from the second part of this Rule as well as from Rule 20 that the event which is the proximate cause for the liabilities, costs or expenses should have occurred during the period of insurance, viz. when the ship was entered with the Club, for the cover to be effective. On the other hand, it is not necessary for the liability to have manifested itself during the time of entry.

Problems of establishing the event which forms the basis of the decision for the cover may arise when the entry of the ship has been transferred from one club to another. If the event is obvious, the liability should be covered by the club where the ship was entered when it occurred. If cargo is damaged on a ship for which the entry has been transferred while at sea and the event cannot be established, the liability is often shared between the two clubs in proportion to the number of days of the relevant voyage during which the ship was entered in each club.

2.9 Direct action

2.9.1 The pay-to-be-paid principle

The third paragraph of this Rule confirms the basic and important overriding principle that the cover provided under these Rules is one for indemnity and not for liability. That is not a contradiction of what has been said under 2.3. The cover is for indemnity of a Member when he has discharged a legal liability covered under the Rules by payment to the claimant. There is no obligation for the Club to compensate the Member until he has effected payment to or otherwise satisfied the claimant. This is referred to as the pay-to-be-paid principle or the payment first principle.

This principle has been challenged in different ways. Attempts have been made to establish a separate right for claimants to seek reimbursement of their losses direct from the clubs by direct action.

2.9.2 Direct action by conventions

Direct action can be imposed by international conventions adopted as domestic law by its signatories. In 1964, a legal right of direct action was introduced by the Paris Convention in respect of liabilities for nuclear damage. In 1969, the International Convention on Civil Liability for Oil Pollution Damage 1969 (protocol 1992), made it a mandatory obligation for owners of ships registered in a convention state and carrying more than 2,000 tons of oil in bulk as cargo to maintain insurance to cover the liabilities of the convention and further allows claimants to turn directly to the insurer for compensation. The consequences of these legally extended obligations are covered under Rule 6 Section 1. As of 2019, the following additional conventions which provide for direct actions against clubs are in force: The International Convention on Civil Liability for Bunker Oil Pollution (2001), The Athens Convention relating to the carriage of Passengers and their luggage by Sea 1974 and the Protocol of 2002 (including the equivalent Regulation (EC) No. 392/2009), The Maritime Labour Convention (2006), and The Nairobi International Convention on the Removal of Wrecks (2007). One common denominator is that these conventions contain a certification requirement which means that an approved insurer – of which Group clubs are one – must provide a “blue card” to the flag state who in turn will issue a certificate confirming there is financial security for liabilities under the relevant convention. The certificate should be carried on board. Further information about certificates under the 1969 Convention can be found under 6.1.3.1.7.

2.9.3 Direct action by law

A number of countries have enacted legislation allowing the claimant a right of direct action against the insurer of a debtor who cannot meet his liabilities on account of insolvency or bankruptcy. Claims are sometimes filed directly against the Club based on such legislation when a Member is in financial difficulties. Under Swedish law direct action is only possible regarding liability insurance which is obligatory by law, or if the insured has been declared bankrupt. The Club needs the co-operation of the Member or of his trustee in bankruptcy or liquidator or administrator to put up a defence against such claims. It follows from Rule 10 Section 4 that the Member (or his successor) has an obligation to assist the Club in this respect.

Some states in the U.S.A., among others Louisiana, have enacted legislation to allow direct action against insurers in all kinds of claims not confined to situations of insolvency. Similar laws can be found in other parts of the world, for instance in Puerto Rico. Jurisdictions which allow direct action may regard a clause such as Rule 2 as being contrary to public policy. In most states, however, the courts appreciate and uphold the difference between an indemnity and a liability policy, as for instance in the States of New York and Florida.

In England, the House of Lords determined that a pay-to-be-paid Rule does not offend against the Third Parties (Rights Against Insurers) Act of 1930. However, the position has changed to a certain extent pursuant to the Third Parties (Rights against Insurers) Act 2010. See comments under 3.4.2.

2.10 Pay-to-be-paid

It follows from the pay-to-be-paid principle that a Member who seeks compensation from the Club should be able to provide a receipt or release to prove that he has actually paid the claim.

It is not sufficient for the Member to prove that payments have been made in respect of liabilities covered under these Rules. The purpose of the cover is not to advance money to the Member pending the result of actions against other parties to recover his loss. To be compensated, the Member’s loss must be final or at least reasonably appear to be final. Recovery possibilities available should first be exhausted. A Member must, for instance, collect any contributions due under the Inter-Club NYPE Agreement (see comments under Charterers’ Liability 2.2) before applying to the Club for compensation of his net unrecoverable loss. Only when reasonable efforts appear to be fruitless may the Club compensate the Member’s loss and be subrogated to his recovery rights under the charterparty through the application of Rule 14. See comments under 14.2-3.

A Member can suffer a provable loss by a claimant either withholding the claim amount from freight payments, or offsetting it against other sums due to the Member. Any such conduct should immediately be brought to the Club’s attention. Otherwise, the possibilities of recovering the amount withheld may become time-barred or jeopardised. It follows from Rule 10 Section 4 that the Club may reject a claim for compensation if a Member is in breach of this obligation. There are generally several options open to deal successfully with a claimant who tries to recover his loss by way of set-off. Freight due to the Member is a clear and undisputed debt due for payment. A claim, however, has to be considered on the basis of the facts of the case. It may take years before it has been established if and to what extent the claim constitutes a clear debt. In the meantime, any set-off of the claim against freight should be legally challenged. If the set-off is in respect of a claim which is likely to be covered under the Rules, the Club will render the Member full assistance. The Member’s loss will be reimbursed when it has been satisfactorily established that the loss reasonably appears to be, or is, final and that it refers to a liability covered under the Rules.

As appears from the third paragraph of the Rule, the fundamental obligation of the Member to pay first can only be waived with the Club’s express approval. The Club may dispense from the obligation on an ad hoc basis, for instance if it has negotiated settlement of a large claim on the Member’s behalf and it is part of the agreement that the settlement amount should be provided urgently by the Club. This is, however, at the Club’s discretion. It also requires the Member to pay the deductible in advance to the Club. The reason for this is that according to the fourth part of Rule 2, the deductible is not included in the cover afforded by the Club.

2.11 Limitation of liability

2.11.1 Background and meaning of limitation

Most countries have enacted laws by which a shipowner is allowed to limit his liability for the types of claims covered under these Rules. Those laws are based on international conventions. There are two general conventions on the limitation of liability, the 1957 Brussels Limitation Convention and the 1976 Limitation of Liability for Maritime Claims, revised by protocol in 1996 (as amended in 2012). There are also conventions geared to cover special types of claims which contain rules on the limitation of liability. According to the International Convention on Civil Liability for Oil Pollution Damage of 1969, revised by protocol in 1992, the so-called CLC, a shipowner is allowed to limit his liability for oil pollution. See comments under 6.1.3.1.5. Corresponding rules on limitation of liability for injury or death of passengers and loss of or damage to their luggage can be found in the Athens Convention of 1974, revised by protocol in 2002. See comments under 3.5.16.

That kind of limitation of liability is referred to as global limitation. It should not be confused with the right under the Hague or Hague-Visby Rules to limit the liability to a certain amount per package or other units of cargo, which is known as the package limitation. See comments under 4.1.9.3.

It goes without saying that claims of an extent and nature likely to invoke the rules on the limitation of liability should immediately be reported to and be handled by the Club. These comments will, therefore, be confined to the general principles and parts that are important for the understanding of these Rules and the cover they provide.

2.11.2 The 1957 Limitation Convention

The limitation amount under the 1957 Limitation Convention is calculated on the net tonnage of the ship, with the addition of the amount deducted from the gross tonnage in respect of the engine room space. The limitation amount per ton is expressed in Poincaré Francs, the value of which is based on the price of gold. Most signatories of the 1957 Limitation Convention have converted the limitation amounts to Special Drawing Rights called SDR. The value of the SDR is published daily by the International Monetary Fund and is to be found in the information on currency exchange rates.

The limitation amounts under the 1957 Limitation Conventions are:

(a) Claims for loss of life or personal injury – Pf 3,100 or SDR 206.67 per ton.

(b) Claims for loss of or damage to property – Pf 1,000 or SDR 66.67 per ton.

(c) Claims for both (a) and (b) – Pf 3,100 or SDR 206.67 per ton, of which Pf 2,100 or SDR 140 to be exclusively available for (a).

The right to limit the liability under the 1957 Limitation Convention is denied where the loss was caused by the actual fault or privity of the shipowner. Privity means knowledge and consent in relation to any fault, defect or misconduct. Only fault or privity by a limited number of individuals within an owner’s organisation will have that effect on the right of limitation. Such persons include the shipowner himself and anybody to whom his managerial power has been delegated, including the head of the technical, operational or safety functions. Situations where shipowners are denied the right of limitation under the 1957 Limitation Convention may be subject to the general exclusion of cover under Rule 11 Section 1. This would leave a Member with an unlimited liability without insurance cover. Borderline cases may arise where limitation is denied but the fault is still not considered serious enough to exclude cover. See comments under 11.1-5.

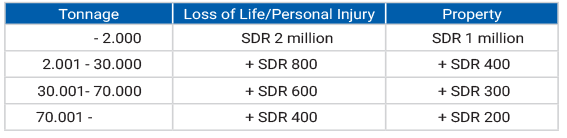

2.11.3 The 1976 Limitation Convention

The 1976 Limitation Convention was brought about by a twofold criticism of the 1957 Convention. Claimants considered the limitation amounts to be too low, whereas shipowners and their Clubs found limitation under the 1957 Limitation Convention too easy to break through.

Under the 1976 Convention the limitation amounts were, therefore, considerably increased. The amounts are:

(a) Claims for loss of life or personal injury to passengers SDR 46,666 per the number of passengers the ship is certified to carry, subject to a maximum of SDR 25 million.

(b) Claims for loss of life or personal injury to persons other than passengers:

tonnage not exceeding 500 tons …………………………………………… SDR 333,000

For a ship exceeding 500 tons, the following sums must be added to

SDR 333,000:

tonnage between 501 and 3,000 tons ……………………………………..extra SDR 500 per ton

tonnage between 3,001 and 30,000 tons ………………………………..extra SDR 333 per ton

tonnage between 30,001 and 70,000 tons …………………………….. extra SDR 250 per ton

tonnage in excess of 70,000 tons …………………………………………….extra SDR 167 per ton

For a salvor not operating from any ship

(or operating solely on the ship being salved): …………………….SDR 833,000

(c) Other claims: tonnage not exceeding 500 tons ……………….SDR 167,000

For a ship exceeding 500 tons, the following sums must be added to 167,000 SDR:

tonnage between 501 and 30,000 tons …………………………………….extra SDR 167 per ton

tonnage between 30,001 and 70,000 tons ……………………………….extra SDR 125 per ton

tonnage in excess of 70,000 tons ………………………………………………extra SDR 83 per ton

For a salvor not operating from any ship

(or operating solely on the ship being salved): ……………………………SDR 334,000

Under the 1976 Limitation Convention, the right of limitation is lost where the occurrence giving rise to the loss was committed with the intention of causing such loss or recklessly in the knowledge that such loss would probably result. A conduct resulting in the loss of the right to limit liability under the 1976 Limitation Convention will most likely render the exclusion from cover under Rule 11 Section 1 operative. This may leave the Member without insurance protection for an unlimited liability. See comments under 11.1-5.

2.11.4 Protocol to amend the 1976 Limitation Convention

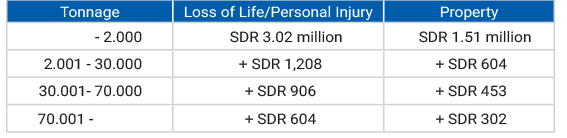

2.11.4.1 1996 Protocol to amend the 1976 Limitation Convention

The 1996 Protocol to amend the 1976 Limitation convention was adopted by IMO in 1996 and entered into force 2006. Under the 1976 Convention, the shipowner’s liability for passengers is limited to SDR 46,666 per passenger with a cap of SDR 25,000,000. Under the 1996 Protocol, the limit was increased to SDR 175,000 per passenger with no upper limit. Furthermore, the limit has to be applied to the number of passengers the ship is authorized to carry according to the ship’s certificate and not to the number of passengers actually on board.

Until the 2012 increase enters into force (see below), the global limitation amounts under the 1996 Protocol remain as follows:

2.11.4.2 2012 INCREASE IN THE 1996 PROTOCOL GLOBAL LIMITATION AMOUNTS

In 2012 an increase in the global limitation amounts adopted by the 1996 Protocol was initiated by IMO member states through the tacit acceptance procedure, a simplified method for adopting new limits under the LLMC. An increase of 51% was agreed as reflecting the changes in monetary values since the 1996 Protocol limits were set. The new global limitation amounts replaced the limits set in the 1996 Protocol in June 2015 and are as follows. They apply to all claims other than passenger claims as follows:

2.11.5 Limitation Funds

2.11.6 Direct action to circumvent limitation

The fifth paragraph of the Rule limits the cover to the sum to which the Member would be entitled to limit his liability. This provision is related to the question of direct action as described under 2.9. In situations of direct action, courts may find that limitation of liability is open to shipowners but not to their liability underwriter. This has created an irresistible temptation for claimants to proceed in direct action against clubs with the sole purpose of circumventing limitation. Therefore, the fifth part of this Rule states that sums in excess of those to which the Member would have been able to limit his liability are not insured.

Rule 30 contains an exception to that principle insofar as certain categories of Joint Members are concerned (see comments under 30.2.2.9).

Affiliated Charterers have a separate limit of USD 350 million (see comments under 30.4.3).

The problem does not arise under the 1976 Limitation Convention, which also applies to insurers of liability for any claim subject to the Convention.

2.11.7 Limitation renders a very high limit of insurance cover

The reason shipowners have been granted the right to limit their liability is because the operation of ships is a high risk undertaking. Limitation of liability will encourage development of commercial shipping and make it possible to effect liability insurance at reasonable cost. As the insurance aspect is one of the motives for limitation, this justifies its ranking in this basic Rule.

Limitation of liability has made it possible for the clubs to provide a very high limit of insurance cover (USD 3.1 billion) for the benefit not only of shipowners but also for potential liability victims. A limited liability backed by insurance is better for the public than an uninsured unlimited liability.

This unique feature of P&I cover is not self-evident. The escalating accumulation of legal liabilities feeds an ongoing discussion as to which level is the proper one for P&I cover.

Some risks have a separate limited cover. As appears from the comments to Rule 6 Section 1 there is a limitation of cover under the P&I policy of USD 1 billion per accident or event in respect of oil pollution. Furthermore, the cover for passengers and seamen is capped at USD 2 billion and USD 3 billion respectively, see Appendix II Rule 1.

2.12 Cover does not include the deductible

The fourth paragraph of the Rule states that deductibles fixed by the Club or agreed between the Club and the Member, are not included in the cover afforded by the Club under these Rules. They constitute amounts for which the Member remains self-insured. For further comments on deductibles, see under 22.5.

The applicable deductible is usually subtracted by the Club before compensation is paid to a Member who has settled a claim under the pay-to-be-paid principle (see comments under 2.9.1). Where the pay-to-be-paid principle has been set aside, for instance in direct action (see comments under 2.9) or where the Club has exercised its discretionary right to provide security (see comments under 12.1), the Member is required to pay the deductible to the Club when security is posted.

As regards exclusion of cover for deductibles under other types of insurance, see comments under 11.6.4.

2.13 Subsidiary sources of insurance information

The sixth paragraph of this Rule records the fact that these Rules are subject to the Articles of Association that form the legal basis under which the Club is allowed to operate. The Articles of Association are available on the Club’s website and they are also attached to the Rule book.

That part of the Rule also states that Chapter 1 (General Conditions) of the General Swedish Marine Insurance Plan of 2006 (SPL) and Swedish law apply in relevant parts in matters not provided for in these Rules. SPL and any other applicable Swedish legislation thus provide supplementary regulations on issues where these Rules may be silent.

SPL was drafted on the basis of the Norwegian Plan. It contains agreed general guidelines on marine insurance matters. SPL is governed by the Swedish Insurance Contracts Act of 2005. Certain terms of that act are of a mandatory nature and have been considered when drafting these Rules. A Member who wants information on SPL or on applicable Swedish law, including the Insurance Contracts Act of 2005, may contact the Club.

Being a Swedish company, The Swedish Club operates under Swedish law. This is reflected by the last part of the Rule, which makes Swedish law decisive in matters not otherwise provided for in these Rules. This principle is the principal reason for the opening part of Rule 1, according to which the Swedish wording of these Rules will prevail. Rule 18 states that disputes under these Rules should be decided in Sweden in accordance with Swedish law.

2.14 Amendment of Club Rules during the policy year

The seventh paragraph provides that the Club can amend these Rules during the policy year to protect the Club against sanction or prohibition by any state or organisation as a result of the operation of an entered ship. By way of example, when EU and USA issued sanctions against Iran in 2010, those sanctions targeted insurance companies that covered vessels engaged in shipping Iranian petroleum products. Sanctions or prohibitions can be directed against the Club as an insurer or reinsurer of an entered ship and can expose the Club to very high fines. In such a situation the Club must have the possibility to adjust the Rules so that it does not provide unlawful insurance cover. The purpose of the Rule is to protect the assets of the Club for the common interest of all Members entered in the Club. It should be noted that the Rule is not limited to sanctions against Iran but instead it can apply to any sanction or prohibition imposed by any state or organisation. Further comments about sanctions and insurance cover can be found under 11.4.1.

It should be noted that that the Club may issue general or particular regulations according to Rule 10 Section 3. Such regulations may also affect the scope of cover during the currency of a policy year, see comments under 10.3.1.

2.15 Personal data

The last paragraph concerns the Club’s handling of personal data. The provision follows from obligations under the EU’s General Data Protection Regulation which is mandatory law in Sweden. The paragraph serves to inform Members that the Club handles personal data according to its integrity policy which can be found on the Club’s website. The Club has legitimate interests to handle personal data in order to fulfil its obligations under the insurance contract. The Member, on the other hand, has an important obligation to inform its employees and representatives that their personal data can be transferred to the Club and handled in accordance with its policy.