Commentary: Rule 22 Premiums and deductibles

22.1 General

The first part of this Rule states that premiums and deductibles for the policy year are decided annually by the Club.

The premium level is decided by several factors. Firstly, a general increase of the premium may be warranted by increased liabilities (for instance through newly adopted international conventions), by inflation or by the Club’s underwriting result. Other elements which should be taken into account are the Club’s anticipated investment income, reinsurance costs, payment of pool claims and the Club’s budgeted overheads and running expenses. The Member’s loss performance as reflected by his record may also necessitate an individual adjustment of the premium.

General increases are decided by the Club’s Board. Notice of general increase decisions is generally given to Members in the head circular issued before the policy year begins.

Individual adjustments are decided upon at the renewal discussions between the Club and the Member, where full and agreed records and statistics are presented. The general increase is applied to the Member’s premiums before any individual adjustments are made.

22.2 Advance calls and additional calls

At renewal discussions, which take place before the policy year has started, it is impossible to quantify with any degree of certainty what final impact the many decisive factors mentioned under 22.1 will have on the actual premium level. P&I Insurance is, therefore, quoted on an estimated total call (ETC) basis. Rule 23 allows the Club to charge Members one or more additional calls should the figures prove, as the policy year develops, that more money is required to meet expected commitments.

22.3 Premiums

22.3.1 Premiums at entry

The premium is based upon the Member’s records, which reflect the Member’s performance during the last five years compared to the premiums paid for those years. For a new Member or for a new ship there are no records available on which the premium can be based. Therefore, when the entry is a transfer from another Club, the loss records from that Club should be presented. In addition to that information, the Club must form an opinion on the liability exposure by evaluating information presented on the type, the age and the condition of the ship, the manning and management status and the trade and cargoes to be operated.

Premium structure

The Club will compare the premium level with that of other Members operating similar ships in comparable trades.

The concept of mutuality between clubs means that premiums should mirror the costs of shared liabilities. Rate cutting to attract more business would violate that principle and allow one Member to enjoy lower premiums at the expense of others. To avoid this, the International Group Agreement (the “IGA”) was drawn up in 1981 by the Group Clubs. It still applies, with certain amendments.

The purpose of the IGA is to restrain competition on rates and leave the Clubs to compete for business on other grounds, such as the quality of their services and stability of their calls.

The IGA contains special rating provisions by a Club, of ships which have been newly acquired by a Member and whose fleet is already entered with another Club, and regulates the situation where a fleet is divided between two or more Clubs. the new Club, to which the vessel is entered, is obliged to follow the terms of entry which would have been offered by the old Club (“the holding Club”) and may not ameliorate terms or apply a lower rate.

The same principle applies in respect of vessels that are transferred from a holding Club to a new Club.

After twelve months, the new Club and the Member are free to make any justified amendments to the terms of entry.

As of 1999, all Clubs in the International Group have to publish their Average Expense Ratio (“AER”) based on an agreed formula in the Group. The AER provides additional information of the cost for services of the different Clubs.

22.3.2 Premiums at renewal

A Member should pay a premium which reflects the risk potentials of the entered ship. Too low a premium means that he is being subsidised by the Club’s other Members. If the premium is too high, he is the subsidiser. Striking the right balance is not always straight forward.

At the time of renewal, experience has been gained and records are beginning to be built up. Then it is easier to determine any adjustment of the premium level to achieve the goal of a realistic estimated total call.

22.3.3 Premiums when cover is terminated or has ceased

When the period of insurance is terminated according to Rule 26 or a Member ceases to be insured under Rule 27, the premium is due to be paid up to and including the date of termination and cesser.

22.3.4 Premiums based on Gross Tons (“GT”)

When premiums are based on GT, the GT is measured as per the International Convention on Tonnage Measurements of Ships 1969.

22.3.5 Payment of premiums

22.3.5.1 Payment dates

The premium is due for payment in four equal instalments: 25% of the premium should be paid on 20 February; 25% on 20 May; 25% on 20 August; and 25% on 20 November.

22.3.5.2 Payment on time

As described under 13.1, the concept of mutuality requires all Members to pay their premiums on time. Return on investments from premiums paid is an essential part of the Club’s income and an important tool to help keep premiums low.

That the premium is due means that the money should be available for the Club on the prescribed payment dates in accordance with the payment instructions contained in the premium invoice or as otherwise agreed by the Club.

22.3.5.3 Payment in policy currency

The premium should be paid in the currency specified in the premium invoice. Payment in any other currency does not constitute payment in full unless otherwise agreed by the Club. Payment in the wrong currency may have the effect described under 22.3.5.5.

22.3.5.4 Set-off

It follows from Rule 13 that the Club has a right to set off unpaid premiums against any amount due to the Member under these Rules or under any other policy issued by the Club.

22.3.5.5 Effect of unpaid premiums

According to Rule 26, the Club may terminate the period of insurance on three days’ written notice if the premium is not paid without delay. See the comments under 26.5.

22.3.5.6 Payment of other sums

Payment of other sums due – such as premiums for accessory types of insurance, deductibles or Club outlays on the Member’s behalf for costs or expenses – should be made on demand and as stated in the instructions.

22.3.5.7 Interest

If payment of premiums and other sums are not received on the due date, the Club may charge interest of 1 per cent per month of the amount due as stated in the current circular. The interest is debited per calendar quarter.

22.3.5.8 No lien

The continuation of cover by payment of the premium due is not an internal matter between the Member and the Club. It also concerns third parties affected by the cover for compulsory liabilities, for instance for crew, cargo and pollution. On 12 March 1999 the new International Convention on Arrest of Ships was adopted. For the purpose of the 1999 Arrest Convention, claims for insurance premiums – including mutual insurance calls – constitute a maritime claim which gives rise to the right to arrest a Member’s ship or other assets.

22.4 Records

22.4.1 Reserves

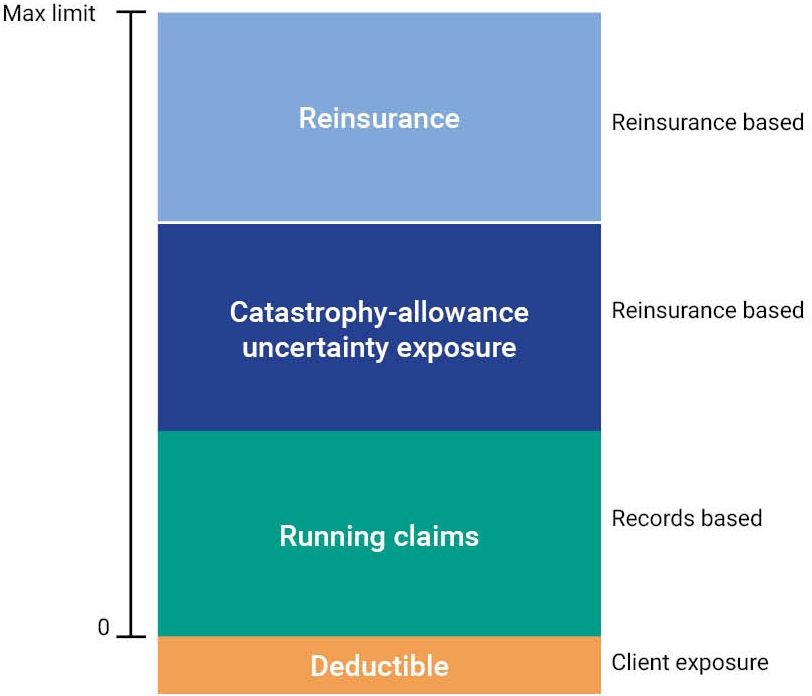

A Member’s premiums are based on his record. The record depends on the aggregate of reserves allocated to cases reported to the Club in connection with the entered ship.

Once a case has been reported which seems to be of a nature to fall under these Rules and which may give rise to a claim for compensation from the Club or cause expenses for investigations or defence, the Club must earmark an adequate amount of money to meet those obligations and costs. As the case develops, estimates of expected costs are replaced by the actual costs as and when they are paid and adjusted, if necessary.

The ideal estimation of a case should predict the total amount of money to be spent by the Club on that particular case when the file is closed several years later. The final outcome is affected by a considerable number of separate factors, which are difficult to predict and quantify. An estimation is always uncertain and vulnerable to criticism. Nevertheless, the Club has the obligation to reserve enough money to meet its obligations under these Rules. The Club defines a proper reserve as a conservative estimation on the basis of known facts of the most likely end result.

All open file estimates are reviewed at least four times a year.

22.4.2 Adequate reserves require notification of claims to Club

If follows from Rule 10 Section 4 that the Member has an obligation to notify the Club when a casualty has occurred or a claim has been made which may give rise to a claim on the Club. Rule 15 contains regulations as to the time within which such notification should be made. Failure to report a claim under Rule 10 Section 4 may cause the Club to reject or to reduce a claim for compensation. The effect of the time bars under Rule 15 is that the claim for compensation becomes extinguished. See the comments under 15.6.

The reason why failure to report or the late reporting of claims is subject to such severe sanction is that accurate records are the cornerstone for the determination not only of the Member’s but also of the Club’s financial position under this insurance.

The premium is based on the Member’s records during a period of five years starting from and including the last completed policy year. Late reporting of a claim reduces the number of years under which that particular claim has an influence on the Member’s records. It causes inadequate premiums to be charged to the detriment of other Members.

The five year claims record can be found on Swedish Club On Line (SCOL). Members are recommended to discuss outstanding claims and reserves with the Club’s claims handlers well in advance of each renewal.

22.5 Deductibles

22.5.1 What is a deductible?

It follows from the fourth part of Rule 2 that a deductible is an amount agreed between the Club and the Member which is not included in the cover afforded by the Club. See the comments under 2.12.

22.5.1.1 What is the purpose of a deductible?

Insurance protects the Member against unforeseeable heavy costs. Minor claims or expenses can be calculated in advance as running expenses. A deductible serves the purpose of keeping such expenses out of the insurance system.

To remit money costs money. Minor expenses do not justify the administration for the Member to compile accounts, for the Club to examine them and for both parties to handle the payment of the compensation due.

A balanced deductible leaves the Member with a stake in the claim. It gives the Member an increased interest in preventing the casualty from arising and in co-operating in the efforts to reduce or reject the claim.

As an example, a Certificate of Entry may state that a double cargo deductible will apply where, in the Association’s view, the cargo claim results from a lack of proper maintenance.

22.5.1.2 How should deductibles be decided?

Deductibles should be balanced against the risks to which they are applied. Large risks which seldom materialise might carry high deductibles. For more frequent risks, the deductibles should reflect the Member’s ability to handle and finance claims below the deductible.

Deductibles which are too high often create difficulties and disputes in the handling of claims, especially when it comes to payment of fees and expenses charged by representatives and lawyers who have acted on instructions from the Club, but at the Member’s expense.

A word of caution may be justified against the practice of using deductibles as an element of underwriting. At premium discussions, a Member may wish to trade a justified premium increase against an increase in the deductible. This may create deductibles which lack proper adaptation to the risks insured and which are unbalanced in relation to the Member’s claims handling and payment capacity. This is neither in the Member’s nor in the Club’s interests.

As appears from the first part the Rule, the deductibles are decided annually. This means that the Club and the Member every year are free to decide on what deductibles are appropriate.

22.5.2 One event can generate several deductibles

No risk is compensated without deductible unless otherwise stated or agreed. The issue whether one or several deductibles should be applied, varies depending on the type of event.

Regarding the obligation to pay compensation, costs or wages to crew under Rule 3 Sections 1 and 2, the deductible is applied per event. An event can be defined by either the obligations in respect of all crew members who sign off on account of injury or illness in a certain port provided that the cause of the disembarkation is the same, or the obligations in respect of the injury, illness or death of an individual crew member, regardless of where he left the ship. This is an important distinction since there may be one illness case and one injury not related but referring to the same port of disembarkation of two crew members. In that event two cases will be registered with one deductible applicable to each case.

For liabilities connected to loss of life, personal injury or illness under Rule 3 Sections 5 and 7 i.e. liabilities in relation to passengers and “others”, the deductible is applied per event considering the cause of the injury, illness or loss of life.

The cargo deductible is set per voyage. A voyage starts when loading commences in the first load port and ends when the last consignment has been discharged in the last discharge port. This means that all cargo claims paid on one voyage should be added together and the same file should also include any cargo related fines. The Member will thereafter be compensated for the total amount less the applicable deductible. When applied to oil spills under Rule 6, the deductible applies also to fines related to pollution under Rule 7 Section 6.

One event can also give rise to several liabilities covered under separate rules. An explosion on board may cause personal injury and loss of life to crew, longshoremen and passengers, loss of or damage to cargo, oil pollution, wreck removal and fines. Each liability will be subject to an agreed separate deductible. Unless otherwise agreed, the individual deductible of each risk involved should be applied to the compensation as and when paid to the Member.

22.5.3 Costs in cases below the deductible

Payment of the premium entitles the Member to cover under these Rules and to service by the Club in the handling of cases arising. The Club and its organisation is at the Members’ disposal at no further charge. Fees charged by the Club’s representatives, lawyers, surveyors and experts are paid by the Club without deductible unless otherwise stated or agreed.

It is a condition that the representatives, lawyers, surveyors or experts have been appointed by the Club and remain under the Club’s instructions.

Expenses paid will burden the case on which they have been spent. They will affect the Member’s record. See the comments under 22.4.1.

What has been stated above applies to cover on general terms. For cover on special terms, it should be agreed between the Member and the Club who should pay for costs of this nature. This is particularly important for Members who wish to carry large deductibles on a per claim basis. It may be appropriate that the Member pays the handling expenses for claims below the deductible and that the deductible is applied to the costs and the liabilities or their aggregate.

22.5.4 Deductibles under other insurance

As stated under Rule 11 Section 6, there is no cover for deductibles borne by the Member under any other insurance.