Section 5 War risks

11.5.1 General

This provision contains the important exclusion from cover of war risks. It applies to war risks in peacetime. In case of the outbreak of a major war or a war involving the state of registry of the entered ship or the state where the insurance company is domiciled, the insurance may be terminated. The effect of such a situation on insurance with the Club is dealt with under 11.5.8 below.

Item (a) of this provision lists a number of general situations, the consequences of which are excluded. Items (b) and (c) identify specific instances where cover is excluded regardless of whether the situation under (a) exists.

11.5.2 Exclusion concerns all risks covered

The war risk exclusion under this provision applies to all risks insured under these Rules such as liabilities in respect of persons, cargo and pollution. As appears from the first part of the provision, a causal connection between the war and the loss is required for the exclusion to take effect.

11.5.3 War and war-like situations

Under item (a) in the first part of this provision cover is excluded for liabilities, costs or expenses arising from loss, damage, injury, illness, death or other accidents caused by war, civil war, revolution, rebellion, insurrection or civil strife arising therefrom or any hostile act by or against a belligerent power.

The application of any of the situations listed has to be made on the characteristics of the position at hand. There are situations of riots or civil commotion of an extent and nature not serious enough to involve any of these situations. On the other hand, it is not a prerequisite for the exclusion to apply that there has been a formal declaration of war. The Group clubs monitor closely the political and military situation in different parts of the world. Members are recommended to stay in contact with the Club when trading in areas where political unrest is current or expected.

In most cases, the carrier should not be held liable for loss of or damage to cargo caused by acts of war by application of Article IV rule 2 (e) of the Hague or Hague-Visby Rules. All contracts of carriage for cargo and passengers should contain suitable war risks clauses. In the absence of such clauses, Rule 10 Section 2 may leave the Member without cover.

By virtue of Rule 10 Section 3 the Club may issue trading warranties which exclude trading in certain areas where war or warlike conditions exist, or allow trading only on payment of an additional premium. The Club may reject or reduce a claim for compensation under these Rules if the Member is in breach of such regulations. It may even cause the insurance to be terminated according to Rule 26 (c).

11.5.3.1 Terrorism

Piracy is by definition committed for private motives. If the use of violence is motivated to achieve political aims, it is widely regarded as terrorism. Such acts are not subject to item (b) of this provision but to the exclusion under item (a). Liabilities, costs or expenses incurred by a Member if his ship is hijacked by terrorists or otherwise exposed to an attack or attempted attack by terrorists are not covered under these Rules. Shipowners usually take out Hull War Risks cover which includes terrorist acts.

If there is a dispute with a Member as to whether or not a terrorist act has taken place the Club will in its sole discretion decide that dispute and the decision will be final.

The taking of hostages by terrorists is a risk not covered. Any liability consequences for instance in respect of passengers will have to be considered by application of the discretion under Rule 19, the Omnibus Rule.

11.5.4 Capture or seizure

11.5.4.1 Exclusion of cover for capture and seizure

Item (b) excludes cover for liabilities, costs or expenses arising from loss, damage, injury, illness, death or other accidents caused by or by any attempt at capture, seizure, arrest or detainment of the entered ship.

Capture means the taking of the vessel as a prize in time of war. Seizure, arrest or detainment are actions which are, at least initially, intended to be temporary.

The entered ship may be seized or otherwise detained as a consequence of an action, the consequences of which are excluded elsewhere under these Rules such as carriage of contraband or employment in an unlawful trade under Rule 11 Section 2 (k). In such a case the cover may also cease under Rule 27. All exceptions applicable should be applied cumulatively to the extent they are not overlapping.

On the other hand, a ship may be arrested for a risk which is indeed covered under these Rules. The arrest may have been undertaken by a claimant to obtain security for damage to cargo or personal injury or loss of life. Although the loss sustained by the arrest is excluded under this item, the Member may still have a valid claim for compensation for the risk covered.

The exclusion under this item for arrests underlines the provisions under Rule 12 that the Club has no obligation to provide security to obtain the release of or to prevent the arrest or attachment of the entered ship.

The Hague and Hague-Visby Rules Article IV rule 1 (g) contain an exclusion of liability in relation to cargo, for loss or damage caused by arrest or seizure. See the comments under 4.1.8.7.

11.5.4.2 Barratry

There are two exceptions from the exclusion.

The first is for barratry, the liability consequences of which are covered. Barratry means a criminal, fraudulent or similar wrongful act undertaken by the Master or crew contrary to the interests of the shipowner.

Barratry can be the intentional scuttling of the entered ship or a mutiny. A condition for cover is that the barratry was committed without the consent or knowledge of the Member.

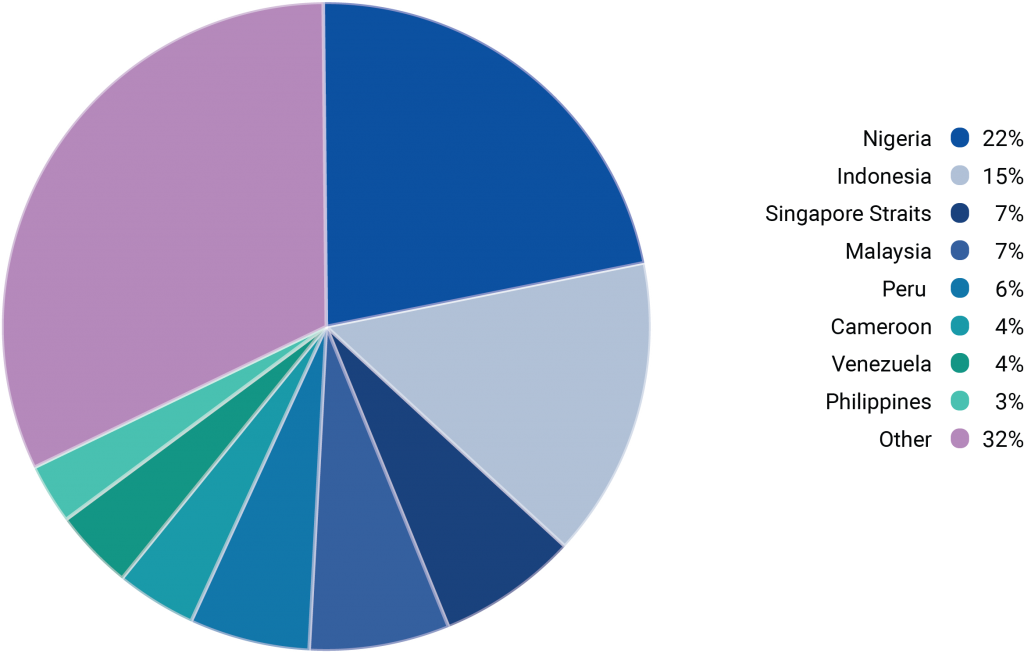

Source: Piracy and Armed Robbery against ships, 2019, ICC International Maritime Bureau

11.5.4.3 Piracy

Piracy is excepted from the exclusion of war risks under item (b) of this Rule and is thus covered by P&I Insurance. However as piracy is also covered by the War Risk policy the P&I Insurance is subsidiary to that cover (see the comments under 11.6) unless piracy is excluded from the War Risks Policy by the incorporation of the Institute War and Strikes Clause (in which case piracy will be covered by P&I Insurance), subject to whether the pirates are using weapons of war as described under (c) of this Rule (in which case it will fall back on war risks cover).

Piracy is defined as an illegal act of violence or detention committed for private motives by persons on a private ship and directed against another ship, person or property on the high seas or in a place outside the jurisdiction of any state. In this respect reference is made to the United Nations Convention on the Law of the Sea (UNCLOS) of 1982.

The International Maritime Bureau (IMB) defines piracy as:

“The act of boarding any vessel with intent to commit theft or any other crime, or with an intent or capacity to use force in furtherance of that act.”

The IMB plays a central role in providing information to the shipping industry about pirate attacks. The Club urges Members to report all actual, attempted and suspected piracy and armed robbery incidents to IMB’s Piracy Reporting Centre. That will help ensure adequate resources are allocated by the authorities to tackle piracy.

The location of piracy attacks varies over with time. In 2010, the vast majority of the attacks took place in the Gulf of Aden and off the coast of Somalia. Following international intervention (see below) and also the use of armed guards, such attacks in the Gulf of Aden have dropped significantly. At the time of writing this text, the majority of attacks are instead taking place in the Gulf of Guinea. Reports of attacks in waters between the Ivory Coast and the Democratic Republic of Congo more than doubled in 2018. Worldwide, the IMB Piracy Reporting Centre recorded 201 incidents of maritime piracy and armed robbery in 2018, up from 180 in 2017.

The Gulf of Aden is in 2019 patrolled by a European Task Force consisting of war ships from various European nations which is assisting ships passing through the Gulf of Aden. War ships from other nations are today also patrolling the area such as Japan and South Korea. Members are recommended to register with the Maritime Security Centre – Horn of Africa (MSCHOA) established by the task force. This website is the best source of regular updated information on the present situation in the area. As regards precautionary measures before entering the Gulf of Aden, Members are recommended to ensure that the latest version of the Best Management Practice to deter piracy is fully implemented. The International Maritime Bureau website contains weekly piracy reports.

The use of armed guards to defend the ship and ship’s crew is a controversial issue. There are many risks inherent in the use of arms on board ships. P&I Insurance does not restrict or prohibit in itself the deployment of armed guards on board but proper care and diligence should be exercised. In this respect Members are recommended to read the Club’s guidelines regarding armed guards on the Club’s website.

Soon after a ship has been seized by pirates a ransom demand is usually made for the release of the ship. A ransom is however not a risk covered by P&I Insurance. A claim from a Member will have to be considered by application of the discretion of the Board under the Omnibus provision, Rule 19. Many shipowners take out Marine Kidnap for Ransom and Hijacking insurance which covers the actual payment of the ransom.

A ransom payment made to obtain the release of a hijacked ship is, however, generally accepted as a General Average expense for which shipowners are entitled to recover contributions. Contributors in GA include all those with a financial interest in the venture, typically: shipowners, cargo owners and potentially Charterers.

In most cases, the shipowner would not be held liable for loss or damage to cargo caused by an act of piracy against the ship. The shipowner should be able to invoke the exception under Article IV rule 2 (f) of the Hague or Hague-Visby Rules.

11.5.4.4 Other attacks

Attacks other than piracy as defined under 11.5.4.3 are frequent and constitute an increasing problem for shipping.

Those attacks take place while ships are proceeding at reduced speed in coastal waters, are at anchor off the coast or lying moored at a quay. Armed robbers enter the ship in order to steal from its cargo or to take cash or articles belonging to the ship or its crew. The Singapore Strait, West African and South American ports are notorious for such attacks.

A Member is covered under these Rules for the liability consequences of an attack or attempted attack of this nature against the entered ship.

11.5.5 Weapons of war

11.5.5.1 Exclusions of cover for weapons of war

Regardless of whether a situation as described under item (a) exists or not, liabilities, costs or expenses arising from loss, damage, injury, illness, death or accidents caused by mines, torpedoes, bombs, rockets, missiles, shells, explosives or other similar weapons of war are excluded under item (c).

The exclusion of liabilities caused by bombs or other explosives means that there is no cover for the consequences of a bomb threat. Loss of time, freight or other revenue during the time the ship is immobilised are excluded under Rule 11 Section 2 (j). Ransom demanded or costs to remove or defuse bombs cannot be compensated by the application of Rule 8 Section 2 as liabilities caused by a bomb threat do not constitute a risk insured. This leaves a Member to seek compensation under Rule 19, the Omnibus Rule.

For the exception to apply, the ship does not need to have been in contact with the explosive devices. Blast damage or other transmitted damage is also excluded.

The nature of the weapons listed implies that the consequences of the use of small arms such as rifles and pistols is covered unless the use on board is part of the situation as defined in the exceptions under item (a) and (b).

As regards nuclear weapons see Rule 11 Section 7.

Item (c) identifies two situations in which the exception does not apply. These situations are dealt with below.

11.5.5.2 Carriage of weapons of war as cargo

The exclusion of cover under this item does not apply to liabilities, costs or expenses arising solely by the carriage of weapons as cargo whether on board the entered ship or not.

For comments on the cover for dangerous cargoes see under 4.1.11.4.

Rule 10 Section 2 may also be applicable as the carriage of dangerous cargoes should be performed under contracts which secure all limitations of and exceptions from liability available to the carrier for the carriage in question.

The exclusion of cover under item (c) does not apply to liabilities arising out of a collision with a warship or a ship carrying ammunition or other weapons of war as cargo.

11.5.5.3 Weapons of war used to mitigate loss

The second part of item (c) deals with the situation where weapons of war have to be used against the entered ship to sink her in order to avoid or mitigate liabilities, costs or expenses covered under these Rules. The ship may be leaking or on fire with a pollutant, explosive or toxic cargo on board. It may also be possible to take similar action against the entered ship as a part of wreck removal activities.

In addition to the requirement that the purpose for using weapons to sink the ship must be to avoid covered liabilities, the action must have been carried out on the order of governmental or other competent authorities, or to have been approved by the Club. According to Rule 1, approval is given in writing.

This part of the provision is the application, to a specific situation, of the general principle contained in Rule 8 Section 2.

11.5.6 Effect of Member’s negligence

The last part of the provision states that the exclusions apply even if negligence on the part of the Member, his servants or agents contributed to the liabilities, costs or expenses.

There may be situations where the proportion of the negligence is so dominant and the contribution of war risks correspondingly so small, that the application of the strict war risk exclusion seems unreasonable. If so, the Member can make an application to the Board to consider compensation under Rule 19, the Omnibus Rule.

11.5.7 P&I war risk insurance

The fact that war risks are excluded from cover, does not mean that these risks cannot be insured or are not insured. On the contrary and as is stated on the head circular issued annually, there is a separate P&I War Risk Cover provided to all Owner Members automatically and at no extra charge.

11.5.8 Outbreak of a major war

11.5.8.1 Swedish flag vessels

What may happen in case of the outbreak of a major war is described in The Swedish Club Outbreak of War Clause (P&I) 1982-01-01 which forms part of the insurance conditions for all Swedish flag vessels.

The Swedish Club outbreak of war clause (P&I) 1982-01-01

Should normal communications between Sweden and other countries be interrupted subsequent to the outbreak of a war which will greatly affect Swedish trade, commerce and industry, an organisation in the name of Svenska Transportförsäkringspoolen (hereinafter referred to as The Pool), formed by all the Swedish Marine Insurance Companies, will commence operations on a date to be decided upon by the Government War Risks Insurance Office.

Should this occur during the duration of this policy, the liability of the Association according to this policy will be transferred to The Pool as from the date upon which The Pool commences operations. The policy will then remain in force and subject to the same terms until 12 o’clock midnight on the thirtieth day of acceptance of liability by The Pool, unless it has been agreed to terminate the validity of the policy at an earlier date.

In the event of the liability terminating prior to the date indicated in the policy, the Assured is entitled to a refund from the Association of the excess premium paid. If on the other hand, the validity of the policy is to be maintained during a period for which no premium was paid, the Assured shall pay premium pro rata parte for this period.

When the above mentioned contingencies arise, it will be incumbent upon the insured to notify the Association or The Pool without delay of the position and the voyage of the vessel.

11.5.8.2 Non-Swedish flag vessels

The procedure of cover described in The Swedish Club Outbreak of War Clause (P&I) 1982-01-01 under 11.5.8.1, applies to Swedish flag vessels only.

For non-Swedish flag vessels the Club may terminate the insurance by application of Rule 26 on the outbreak of a major war.

The arrangement of new cover will depend on the market situation and any applicable regulations in the ship’s state of registry.